Decentralized Finance: An Explosive New Paradigm Challenges Existing Finance Systems

Decentralized finance (DeFi) is an extension of the original use case for cryptocurrency and digital assets: a means to transact value without the interference of third party middlemen or governmental systems. While digital assets have performed well in peer to peer transactions, performing wider services such as credit and lending have since eluded cryptocurrency developers. As the pandemic has constrained access to credit and caused banks to lower interest rates, customers have begun searching for alternatives, leading to the explosive growth of decentralized currency; banking services provided more cheaply and transparently on the blockchain.

How DeFi Can Outmaneuver Existing Financial Systems

The front and center use case for decentralized finance is the fact that it has no key point of failure. Banking institutions have an unfortunate coupling of characteristics in that they are absolutely fundamental sections of a nation’s infrastructure and also extremely vertical, top-heavy organizations. Should a bank fail, whether it is for reasons of greed, malfeasance, or simple incompetence, it can have a horrific impact on not only its former customers but other financial systems connected to it, evidenced during the Great Depression in the form of bank runs and later the Great Recession spurred on by the subprime mortgage crisis. On a more individual scale, banks can seize or freeze assets or close accounts for any reason or no reason at all, especially in totalitarian or censorship-heavy countries. DeFi is built on public blockchains, open to anyone, with no human element having a hand in how funds are managed, removing certain corrupting influences found in traditional banking institutions.

Further, DeFi provides unique competition to current institutions that cannot be bought, broken up, or pushed out of the market. Obtaining loans without a credit record is extremely difficult, and sending remittances cross-border is expensive, yet due to the way these institutions are structured creating a competing service using traditional means can be prohibitively expensive. DeFi, therefore, cannot be ignored as a challenge to traditional banks.

The idea behind DeFi is not completely new in the digital asset sphere, but recent adverse financial conditions spurred on by the pandemic have created lightning in a bottle. Customers are fed up by falling interest rates and tightening credit options and since banks tend to all act very similarly in response to the market, customers also feel stymied by the lack of alternatives. With new options to bypass the traditional system and allow creditors and borrowers to connect directly to hash out their contracts without a middleman’s interference, a new paradigm was born.

The Technical Means Behind DeFi

Contrary to traditional banking systems, a properly written decentralized finance app – also known as a DAPP – is open-source, transparent, resides on a public blockchain, and is globally reachable. DAPPs require little human intervention and are built on smart contracts, which are essentially a set of rules programmed to act a certain way given an input, such as when a payment is received. More complicated systems can be built such as decentralized exchanges that facilitate digital asset trading without the need for a trusted intermediary. As these exchanges are more automated and require less maintenance than traditional exchanges, they are often cheaper to trade on. To provide a level of surety, DAPPs often involve the use of stablecoins, which represent a digital asset pegged to a real-world asset that can be sent via the blockchain.

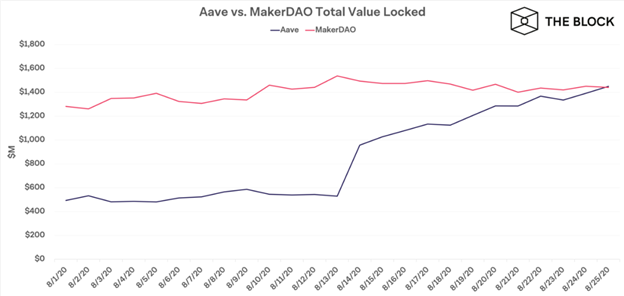

Several categories of DAPPs already exist to mirror traditional banking functions, including options for payment, infrastructure, exchange, credit and lending, and investment, as well as for commerce such as peer to peer marketplaces, data and analytics, and even lotteries. Some of these offerings have seen heavy adoption, with Aave’s LEND being the star of the show recently being the second DeFi app to achieve $1 billion USD locked on their platform, most of it being deposited in the last two months. Aave has become a major competitor to MakerDAO, the first app to achieve the milestone.

How DeFi Can Benefit Venture Capital Investors

Despite recent declines in venture capital investment in digital assets, decentralized finance is still burgeoning; in April, despite a 57% decline in overall cryptocurrency funding from the month prior, DeFi raised 150% of its total. It’s in an excellent position because there is a lot of motivation behind the idea, and a lot of ecosystem building still needs to be done, meaning there is a lot of space in the market. Digital assets are quite well-known at this point, but up until now the only challenge they’ve provided to traditional banks are peer to peer payments at lower prices. DeFi represents the potential to compete with and even upend the status quo, which has always been at the heart of blockchain, but taken a step further by offering solutions for contracts based on trust, such as lending and insurance.

The inaugural Global DeFi Summit was held this month and provided a lot of insight as to why venture capital is popping off. Michael Anderson, the founder of Framework Ventures opined that the Internet and blockchain innovators will become “the new Goldman Sachs” and that the term “DeFi” will eventually become just “finance.” He tempered this statement, though, by adding that the timescale for DeFi’s growth will be in decades rather than years or quarters. He also felt that traditional banking systems are much overdue for innovation, having not seen major changes in the past 40 years despite being the single largest market in the world. Alon Goren, founding partner at Draper Goren Holm, likened them to “dinosaurs” and that new, more transparent, fairer products will take their place, citing Wells Fargo creating accounts for customers without permission as an incident that would not occur under the new DeFi paradigm. Overall, sentiment is extremely strong in the arena, with the knowledge that a lot of work still needs to be done; a lush, relatively untapped market for potential investors.

Concluding Thoughts

Where DeFi will go from here is largely up to the participants in its ecosphere. Needless to say, the seed has already been planted that institutional banks are in dire need of additional competition, which will shape action going forward. The success cases of MakerDAO and Aave have shown that there is certainly a viable market for investment, and the knowledge that there is work to be done will bring developers to the space to create new investment opportunities.

If you have questions about our fund or would like to be sent investor documents, you can contact our investor relations department at [email protected]/.website_ad411e93.